Fraud protection.

Now it's personal.

ANZ Falcon® technology monitors millions of transactions every day to help keep you safe from fraud.

Falcon® is a registered trademark of Fair Issac Corporation.

Fraud protection.

Now it's personal.

ANZ Falcon® technology monitors millions of transactions every day to help keep you safe from fraud.

Falcon® is a registered trademark of Fair Issac Corporation.

Log in

Explore more

Fraud protection.

Now it’s personal.

ANZ Falcon® technology monitors millions of transactions every day to help keep you safe from fraud.

Falcon® is a registered trademark of Fair Isaac Corporation.

4-minute read

When it comes to saving money, you can be your own worst enemy. Just when you think you’re getting ahead, you withdraw a stash of cash for an unplanned purchase. Hiding your money can help.

There’s actually science behind the idea of hiding your money to help you save. Let’s take a look.

In the 1970s, economist Richard Thaler invited a bunch of mates over for dinner. During pre-dinner drinks, he noticed that they were all tucking into a bowl of cashews. Simply because the nuts were there. Thaler took the bowl away and, surprise, surprise, they stopped eating them.

His lightbulb moment from this accidental experiment was that humans lack self-control. Even though we know the cashews will ruin our appetite, we still grab a handful. Hey, no-one’s perfect, right?

Many people lack self-control when it comes to saving money, too. You know you shouldn’t dip into your savings, but you’re a sucker for sneakers, a softie for smartphones, a goner for gems or a freak for fashion. All is not lost!

Using Thaler’s idea, one of the easiest ways to regain control over your savings is to remove the money from sight. Out of sight, out of mind.

We’ve come a long way from the days when hiding your money meant stuffing an envelope full of cash under your mattress. We’ve also heard stories of people who chuck their credit card into the freezer, so that the thawing time would also melt any possibility of an impulse buy! Yet, these days, it’s so easy to open an online savings account that you’d have to be a Luddite not to.

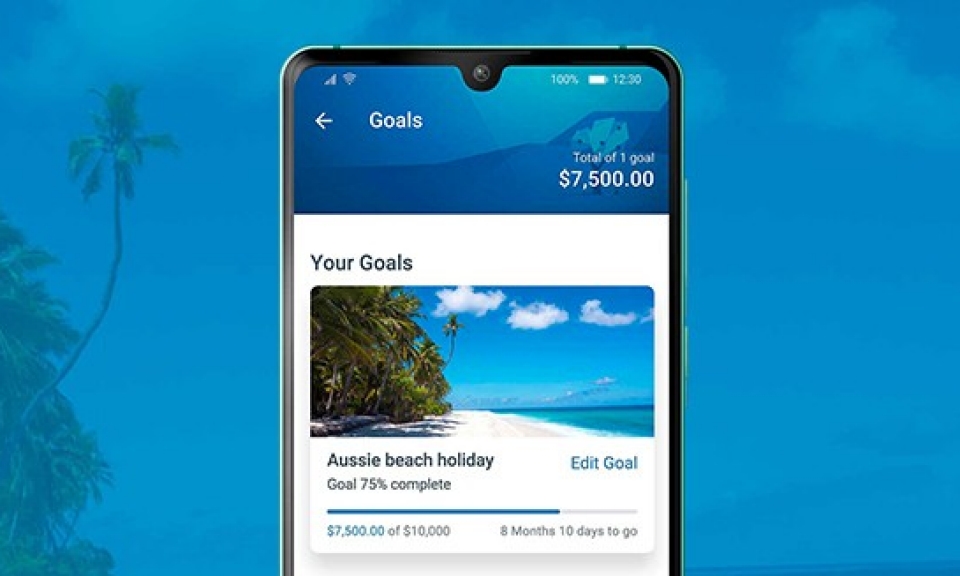

To steer yourself away from temptation, you could consider setting up a separate savings account in addition to your everyday transaction account. Give the account a name that reminds you of exactly what you’re saving for. ‘Forever home’. ‘Burning Man trip’. ‘My wedding day’. You get the idea. If you need an extra deterrent, add a few more words: ‘Do not spend under penalty of death’. If you’re good at following instructions, then you’re on your way to sweet savings.

Once you’ve set up your savings account, you may want to take an extra step: hide the account from view in online banking. Then when you log on to your online banking to pay a bill or check your credit card balance, you don’t see your savings account and you’re less likely to use it.

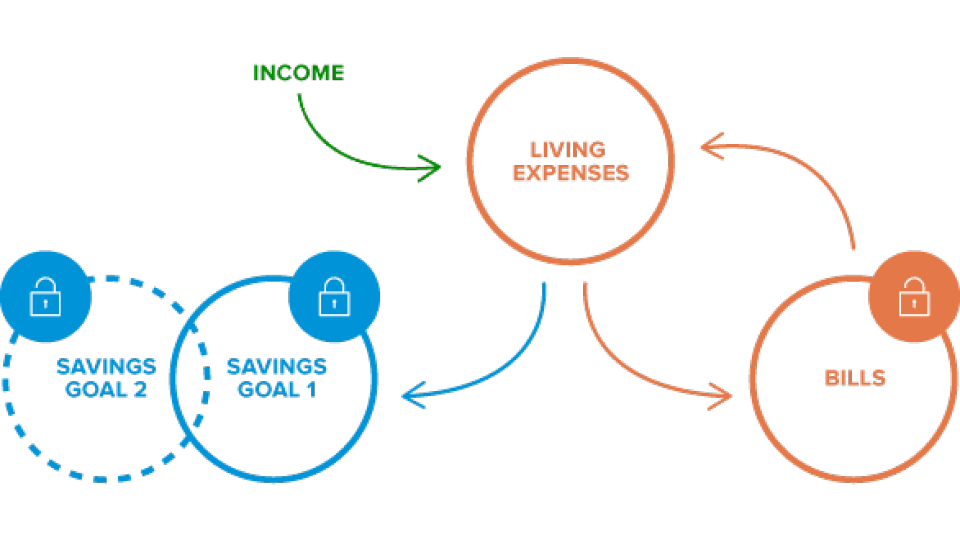

Separate your savings by setting up multiple savings accounts in addition to your your everyday transaction account. Set up automatic transfers so that you scan set and forget. When you have amassed a decent sum, lock it away using a term deposit.

To help your savings grow even faster, turn on auto-pilot. The less you have to think about saving money, the easier it is to save.

For ‘out of sight, out of mind’ savings, jump onto online banking and set up an automatic transfer from your everyday account (or, whichever account your salary goes into) to your hidden savings account. First, work out how much you can afford to save. Even if it’s just $20 a week, you’ll have over $1,000 in your account after one year. Not bad, huh? Then, if possible, set the automatic transfer date for the day after you get paid so you know money is available for the transfer.

With your savings on auto-pilot – safely stashing your money before you have a chance to spend it on macchiatos or muffins – you’re well on your way to your savings goal.

If you already have a decent sum of money – perhaps an inheritance or a work bonus – then a term deposit is a very secure way to hide it. Think of it as the ultimate ‘out of sight’ savings plan.

With a term deposit, your savings are locked away until the term ends. There are usually penalties if you take your money out early, which can stop impulse spending in its tracks.

To help your savings grow even more, tell the bank to roll your term deposit over when the term ends. This way, you’d have to give them notice if you want your money at the end of the term – a good deterrent to spending it. Or, when the term ends, you could add any extra savings that you’ve stockpiled to the lump sum, and start a new term deposit.

One savings trick that might work for you is to make it just that little bit harder to get your hands on your money. This applies to your hidden money, too. Your goal is to add hurdles between you and the cash.

For example, ask the bank to block your ability to withdraw money from your savings account using ATMs; or ask them to pop in an extra step to get at your savings online – like having to come into the branch or call. Sometimes it pays to be lazy!

These little hurdles are all designed to help you pause and ask yourself whether you really want to spend the money you’ve been working so hard to save. Studies show that they work – adding even the smallest amount of effort to get your hands on your savings will reduce the likelihood of you trying.

The bottom line? Hiding your money is about resisting temptation and reducing impulse spending. If you’re saving up for something big, why don’t you give it a try?

The information set out above is general in nature and has been prepared without taking into account your objectives, financial situation or needs. Before acting on the information, you should consider whether the information is appropriate for you having regard to your objectives, financial situation and needs. By providing this information ANZ does not intend to provide any financial advice or other advice or recommendations. You should seek independent financial, legal, tax and other relevant advice having regard to your particular circumstances.