Estimated reading time

5 min

In this article

- Learn how compound interest works

- How to make the most of it

- Superannuation and the benefits of compounding interest

- See some examples and scenarios

![]()

Compound interest can be a real game changer for your savings. But what is it? And how does it affect your finances?

Simply put, compound interest is earning money on your money. And that money earning money on that money. And that has the potential to snowball exponentially. It does the work for you, so you feel like your savings are going in the right direction without much effort.

It might not be widely understood, but it can be pretty powerful when it comes to planning for your future – especially if you start early!

So, how does compound interest work?

With simple interest, you only earn interest on your initial savings deposit. And that interest won’t be added to the closing balance of the account. But with compound interest accounts, it’s a snowball effect on your savings. Essentially, you earn interest on your interest.

How can you make the most of it?

Make sure you choose an account that works for you by considering the account terms and fees, including minimum deposits, interest base rates, and withdrawal fees. Explore your options and use the MoneySmart compound interest calculator to work out how much you’ll need to save each month to reach your long-term goals when you factor in compound interest. The longer you save, the more interest you earn. So, start as soon as you can and save regularly. You’ll earn a lot more than if you try to catch up later.

Keep in mind that inflation might affect the savings you get from compound interest. For example, if inflation is higher than the interest rate on your savings account, your purchasing power might go down over time. Ideally, the interest rate on your savings would be higher than inflation so that you get more value from your money over time.

Super Interesting

Compound interest is a long game, but it’s one worth playing. And if you’re in it for the long haul, super is a great place to take advantage of the benefits.

Super is an easy way to grow your money behind the scenes. Superannuation accounts are set up so that you earn compound interest on your contributions. And once you get going, it’s automatic. Remember, these are long-term savings for retirement so you can’t easily access these funds whenever you feel like it.

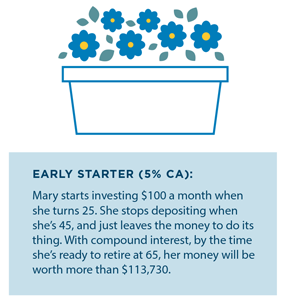

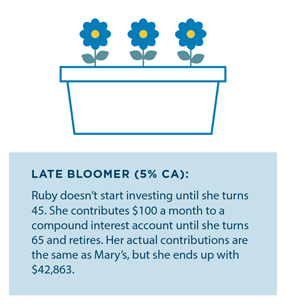

To understand how compound interest factors into your super balance, let’s look at an example.

Say you have $10,000 in your super account to start with. The below shows what happens if you save $50 a week from the age of 20 based on an average 7.5% super return*.

Forecast what you could personally achieve using MoneySmart’s compound interest calculator.

*The returns estimated here are based on MoneySmart’s Superannuation Calculator’s rate of 7.5% in 2024, and do not include fees and charges. It’s important to note that the rate of return can fluctuate from year to year, from fund to fund, and depending on whether you have selected a conservative, balanced or aggressive investment approach.

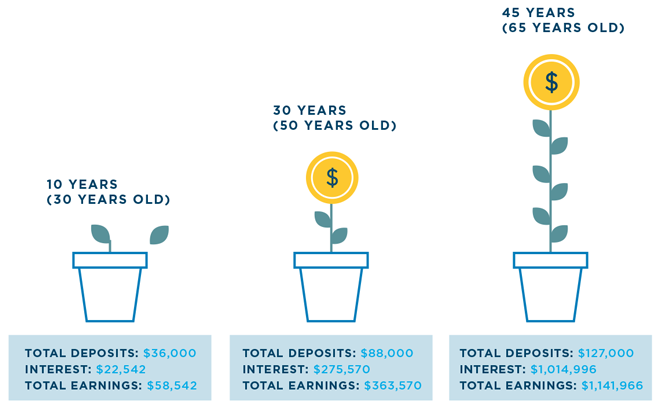

The earlier you start saving, the better

With compounding on your side, every dollar you invest will add exponential value over time. Every year, your interest will increase even if you stop investing. For example:

Brain hack

You’ve saved around $18,000 over five years. Nice job! You might feel proud of yourself and decide to spend your hard-earned savings because it’ll make you feel good. But what if you kept saving for another five years and doubled the savings you had instead? Settling for a smaller reward now instead of the larger future reward is a thought process called ‘hyperbolic discounting’. To avoid this way of thinking and stay on track with your savings, keep your eye on the prize and your long-term financial goals. What are you working towards? And how will future-you feel if you withdraw your savings now?

This will help you to resist the temptation of dipping into your savings and keep the compound interest ball rolling.