Estimated reading time

6 min

Learn all about

- The power of compound interest – what it is and how it works

- Making the most of compound interest

![]()

Saving for the future can sometimes feel like playing the long game.

When budgets are tight and the cost of living somehow keeps climbing, putting money aside regularly and watching the balance grow can feel like a pipe dream.

But did you know there’s this cheeky little tool called compound interest? And the earlier you save, even if it’s a spare dollar or two, the sooner your balance will grow faster and bigger.

So, what is compounding interest?

Compound interest refers to interest you earn on your savings, as well as any interest you accumulate. This can create a bit of a snowball effect. With compound interest, every dollar you invest will add exponential value.

Compound interest works differently to simple interest, where you only earn interest on your initial deposit.

The main factor? Time. The earlier you start saving, the better your compound interest will be.

But how do you start accumulating compound interest and savings?

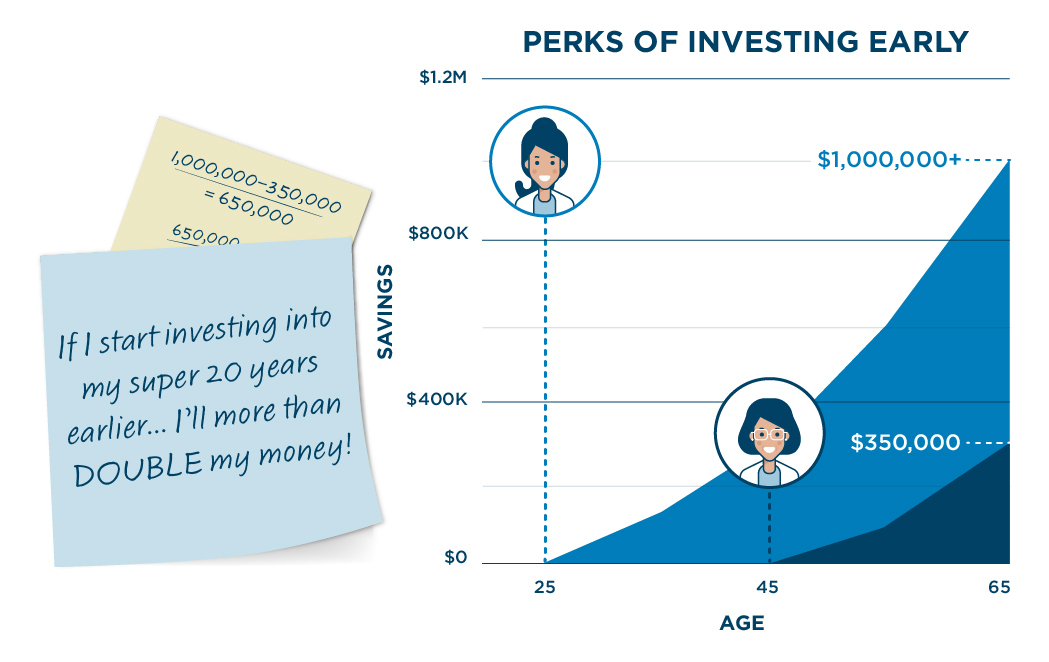

Take the below compound interest formula example: Starting at age 25, Ruby invests $1,000 per month into a savings account that has a compound interest rate of 3.5% per annum. By the time she’s 65, she’ll have more than $1 million in her account.

Think about it like running a race. Even professional athletes don't roll out of bed one day and win the Olympics on a whim. Start now, keep your goals in mind, and dedicate time to checking in. Whether you’re aiming for a home, a holiday, or a comfy retirement, compound interest is one way to turbo-boost your savings with minimal effort.

If you need help to calculate your compound interest, the government’s calculator tool is a great way to see it in action. Now, how do you get started?

Remember to do what’s right for you and your circumstances. Look at the eligibility criteria, terms and conditions and any fees and charges that apply to any savings or investment products. You can also consider seeking independent financial and tax advice.

Step 1: Get the ball rolling and start compounding

Amassing a lump sum is the first step on your investment journey (and remember, long-term savings is a form of investment). In most cases, you’ll need this to invest in higher-return strategies down the line. Finding a savings account that pays a good rate of compound interest can reward you for regular savings. Always check the eligibility criteria and the terms and conditions as some require minimum deposits or for you to not touch them to get interest.

You should also consider various other types of investment (e.g. term deposits or bonds), and seek independent advice to work out what is best for you.

Step 2: Build momentum with compound interest

So, you’ve built a little lump sum, ready to send out into the real world of high-return investments. There are many strategies that put the snowball effect of compound interest into action, including:

Managed Funds. Your money goes into an amalgamated pool with thousands of other investors. A fund manager then invests this money on your behalf in the form of shares or bonds. Different types of managed funds hold varying levels of risk. Usually, the higher the return, the higher the risk.

Exchange Traded Funds (ETFs). An ETF is a managed fund that is listed and tradeable on the stock exchange. They can reflect their real-time value throughout the day, whereas managed funds are priced daily, weekly or even monthly. Essentially ETFs allow beginner investors to quickly and easily enter the market, however, be mindful that a brokerage is charged each time you add more money (as you’re buying more listed securities). If you’re wanting to keep your options open, read up on ETFs.

Bank Deposits. Not keen on branching out into the riskier realm of shares and bonds just yet? Bank deposits may be the way to go. Though they lack the opportunity for exponential capital growth, they help make the most of compound interest closer to home.

According to Rebecca Hurford, our Senior Financial Advisor at ANZ, "The beauty of Managed Funds or ETFs lies in your ability to diversify - spreading your savings across a range of shares, properties and bonds from around the world, not just in Australia. They allow you to start small and build a significant asset for your future."

Always read the eligibility criteria, fees and charges and terms and conditions carefully and consider seeking independent financial and tax advice to ensure you’re doing what is right for you. Different investments have different levels of risk and return that you must understand before getting involved.

Step 3: Supersize your snowball to earn more compound interest

If you’re working in Australia, you’re probably already benefiting from compound interest – even if you didn’t know it. That’s right: superannuation is a compulsory, long-term compound interest tool that’s well known, yet still underutilised.

If you're looking for a way to supersize your superannuation, you could consider some of these hot tips:

Roll your super into a single fund so you’re earning compound interest on a bigger balance

Double check you’re using the best super fund for your goals. The ATO offers a superannuation comparison tool, which measures a variety of performance factors and fees between similar funds

Consider a ‘salary sacrifice’ arrangement where an additional portion of your payslip is invested in your super, before it reaches your bank account

Check eligibility for government co-contribution for lower income earners or ‘spouse contributions’ to your superannuation

Don’t forget to check in: It pays to check in regularly on your investments. Are they meeting the goals you have your eye on? Do you need to speak with a financial advisor to make sure your investments are still working for you? With dedication and a little patience, anyone can start earning interest off their interest – better late than never.